Methodological note

Sustainability performance: Legislative decree no. 254/2016 and GRI standard

Acea has prepared and published the Group’s Sustainability Reports on a voluntary, annual basis, starting in 1999 (for the 1998 financial year), with the aim of integrating economic and financial information with the social and environmental aspects of its activities.

From the early years sustainability reporting has been carried out in conformity with the international reference Guidelines 1, under constant development, and voluntarily submitted for audit and verification by a third party. Moreover, with the intention of providing the financial community and interested parties with a complete disclosure regarding Group performance, the publication times for the Sustainability Report have been aligned with those of the consolidated Sustainability Report as from 2011.

Since the 2017 edition, as is well known, the Sustainability Report has been published in compliance with Legislative Decree no. 254/2016 2, which transposed EU Directive 95/2014 into Italian law. Under the Decree, companies that meet the conditions set out in article 2 are required to publish information on sustainability performance in a non-financial statement – individual or consolidated – which, as stated in the Decree in article 3, paragraph 1: “...to an extent necessary for ensuring an understanding of the company’s activity, its performance, results and the impact it produces, relating to environmental, social and employee matters, respect for human rights, anti-corruption and bribery matters, which are relevant given the activities and characteristics of the enterprise...” 3.

This Sustainability Report, for the year 2018, is the 21st published. It has been prepared in accordance with the GRI Standards (ed. 2016) 4: Comprehensive option and therefore called Acea Group’s 2018 Sustainability Report (consolidated non-financial declaration pursuant to Legislative Decree no. 254/2016, prepared in accordance with GRI standards), taking the form of an autonomous document, as permitted by the aforementioned Legislative Decree 5.

The Sustainability Report, enclosing a Summary Note, following its approval by the Board of Directors, is made available to the supervisory body and submitted for assurance by the statutory auditor, with which Acea has no joint interests or other connections, appointed with verifying the conformity thereof with Legislative Decree no. 254/2016 and its consistency with the implemented reporting Standards 6 (see Opinion Letter of the independent auditor).

The document is made available online on the institutional website at the same time as the Consolidated Financial Statements and distributed at the Shareholders’ Meeting.

1 - After the first years, in which other focuses were also referred to, starting with the 2003 Sustainability Report Acea opted for the guidelines issued by the Global Reporting Initiative (GRI), then in its 2002 edition, in the following years remaining in sync with all the developments, maintaining the highest level of “accordance” possible. Finally, starting with the 2017 Sustainability Report, which also complies with Legislative Decree no. 254/2016, Acea adopted the GRI Standard (ed. 2016), anticipating the requirements of the GRI by one year.

2 - It should also be noted that article 1, paragraph 1073, of the 2019 Budget Law introduces an amendment to Legislative Decree no. 254/2016, art. 3, paragraph 1, letter c, also prescribing the illustration of the methods for managing the main risks.

3 - Legislative Decree no. 254/2016, in particular articles 2, 3, paragraphs 1, 4.

4 - The Global Reporting Initiative (GRI), launched in England in 1997 by the Coalition for Environmentally Responsible Economies (CERES), became independent in 2002 as an official centre supporting the Unite Nations Environment Programme (UNEP) and works in collaboration with the United Nations Global Compact.

In 2016, when the previous version of the Guidelines for Sustainability Reporting (GRI-G4) were superseded and further developed, it published the GRI Standards – Consolidated set of GRI Sustainability reporting standards 2016 – available on the website www.globalreporting.org, requiring their adoption with respect to the 2018 financial year. Acea has anticipated such adoption, with the Comprehensive option, since the 2017 Sustainability Report.

5 Therefore, the Acea Group Sustainability Report 2018 is to be understood as a Consolidated disclosure of a non-financial nature (Legislative Decree no. 254/2016, art. 4 and art. 5, paragraph 3.b).

THE FIRST YEAR OF MANDATORY NON-FINANCIAL REPORTING IN ITALY

2018 was the first year of application of Legislative Decree no. 254/2016, which made annual non-financial reporting mandatory in Italy for about 200 companies. The way in which these companies managed the first year of production of the Non-Financial Declaration (DNF) was the subject of analysis by important observers, who also wanted to further develop some aspects of content and quality.

A first finding from the analyses is that more than 50% of the DNFs examined were produced by organisations that approached the issue of non-financial reporting for the first time. The Energy and Utilities segment, on the other hand, has long been committed to sustainability reporting by virtue of its peculiar line of business (services of common interest, strong presence in the local region, interaction with diversified stakeholders).

In addition, about 80% of the companies surveyed exercised the option of producing a stand-alone document. Among the reporting standards adopted, the GRI was confirmed as the reference for 100% of the organisations examined, although with respect to the use envisaged by the GRI the most popular was the core (about 58%), a high percentage (38%) used the standard only as a reference, while the comprehensive level was only implemented by a few companies (4%).

As far as materiality analysis is concerned, 60% of companies carried out this activity for the first time for the purposes of drafting DNF 2017, while the remaining 40% had already carried it out, although, according to the surveys, this activity was not always structured in defined procedures and responsibilities, involving, for example, the Board of Directors or the Board Committees.

The establishment of internal committees to oversee sustainability issues was another aspect noted that has still been poorly applied, as well as a specific strategic planning: on this point, research indicates that only a minimum percentage of companies – between 13% and 19% – publish Sustainability Plans.

The process started with the first year of application of Legislative Decree no. 254/2016, according to the interpretations of the researchers, as with all new initiatives shows a substantial dual register between companies going through their first experience, more mature companies or major listed companies (FTSE MIB) and minor or unlisted.

However, it seems that the climate is ripe for a decisive acceleration by all companies, each for its own areas of improvement, towards the implementation of corporate sustainability.

Materiality, gri standards and report scope

For 2018, given the stability of the company’s management, the continuity of the Group’s strategic guidelines and the absence of marked changes in the context analysis, Acea confirmed the relevance and validity of the results of the materiality analysis carried

out in 2017. The analysis, aimed at identifying the most relevant – material – economic and governance, social and environmental issues for the company and its stakeholders, taking into account their impacts on the business and on the stakeholders themselves, was in fact renewed last year at every stage: document and context analysis, discussion with stakeholders (internal and external) and with company managers 7, drawing up the schema and reporting the results.

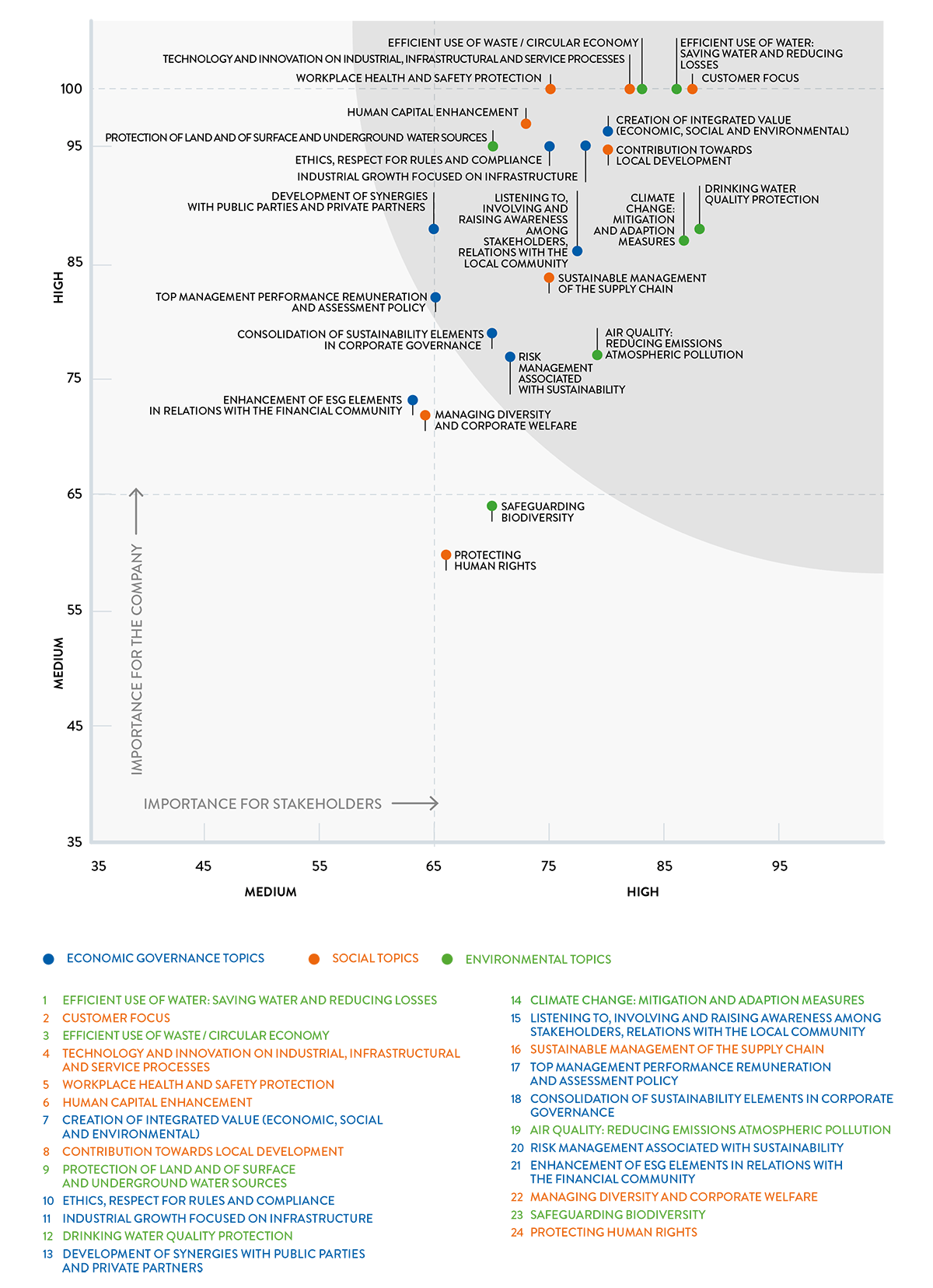

The 2018 materiality schema is therefore unchanged from the one illustrated in the previous edition of the Sustainability Report. This identifies and articulates 20 highly significant topics (score 66- 100) in a Cartesian coordinate system and 4 of medium significance (score 36-65) (see Chart no. 1).

The highly significant matters proved to be consistent with the Group’s strategic planning, regarding industry and sustainability.

The materiality analysis and its results were on the agenda of a meeting of the Ethics and Sustainability Committee in October.

6 - Legislative Decree no. 254/2016, under art. 3, paragraph 10, provides that: “The subject appointed with performing the statutory audit of the Sustainability Report (...) or another subject entitled to performing the statutory audit as specifically designated” issues “a certification concerning the conformity of the provided information respect to the requirements under this legislative decree and respect to the principles, methods and procedures provided under paragraph 3”. Namely principles and methodologies:

“provided by the reporting standard used as reference (...)”.

7 - In particular, as far as the direct comparison with the stakeholders is concerned, Acea organised a multistakeholder focus group in September 2017 with 21 attending organisations representing 13 subcategories of stakeholders, totalling 26 persons, entrusting the performance thereof to an external expert and in October 2017 while the strategic, industrial and sustainability planning was being defined, it organised a board meeting with the corporate management. For an illustration of the materiality analysis carried out in 2017, see the Methodological Note to the Acea Group’s 2017 Sustainability Report, available online on the company’s website: www.gruppo.acea.it.

CHART NO. 1 – RELEVANT TOPICS FOR THE COMPANY AND STAKEHOLDERS: ACEA “MATERIALITY MATRIX” – 2018

The classification of material topics into high, medium or low relevance, as well as being important from the strategic viewpoint, is functional to identifying the aspects to be reported with a higher or lower detail in the sustainability report and selecting the indicators provided under the reference Standards.

To prepare the Sustainability Report in accordance with the GRI Standards (ed. 2016): comprehensive option, in fact, it is necessary to illustrate the performance in light of:

- “Universal Standards”, which include the reporting principles (GRI 101: Foundation) and 56 general standards (GRI 102: General Disclosures);

- the aspects considered to be material (“material topics”) and related indicators, to be selected from among the 33 aspects envisaged in the Standard (“Topic-specific Standards”): GRI 200-Economic, GRI 300-Environmental, GRI 400-Social);

- the management approach (GRI 103: Management Approach) for each aspect deemed as material.

In order to be able to select the “material topics” from among those envisaged under GRI Standards, consideration 8 was given to both their correlation to Acea’s highly significant topics and meaning thereof conferred by the international Standards, in some cases tracing them back to the corporate context and in others establishing their lack of pertinence 9.

Following the assessments described above, 25 Topic-specific standards were identified out of a total of 33, as consistent with Acea material topics of high significance (see Table no. 1), although not always exhaustive in the widest sense of the meaning 10, which is more widely covered in the document where appropriate.

Furthermore, among all the indicators included in the “topic-specific standards” considered as “material”, only 4 were considered as not pertinent and excluded from the analysis. Only one Acea material topic of high relevance is not correlated to the Topic-specific standards, this being the Consolidation of elements of sustainability in corporate governance, which however, is fully consistent with the general standards dedicated to aspects of governance (GRI 102: General Disclosures).

Lastly, also regarding Acea material topics of medium significance present in the report on a less descriptive basis, consistencies were found, albeit not highlighted in the table, with both the “material Topic-specific standards” and the “general standards” (GRI 102: General Disclosures).

TABLE NO. 1 - CONSISTENCY WITH GRI “MATERIAL TOPIC-SPECIFIC STANDARDS” AND ACEA “MATERIAL TOPICS” OF HIGH SIGNIFICANCE

| GRI 200: economic topics 2016 | Acea material Topics | GRI 300: environmental topics 2016 | Acea material Topics | ||

| Economic performance | 4, 6, 7, 8, 10, 11, 14, 17, 19, 20 | Material (301-1) | 3, 4, 9 | ||

| Indirect economic impacts | 2, 3, 4, 7, 8, 11, 13, 16 | Energy (from 302-1 to 302-4) | 4, 9, 14, 19 | ||

| Procurement practices | 7, 16 | Water | 1, 4, 9 | ||

| Anti-corruption | 10 | Biodiversity (from 304-1 to 304-3) | 9, 14, 19 | ||

| Anti-competitive conduct | 10 | Emissions | 9, 14, 19 | ||

| Effluents and Waste (from 306-1 to 306-3, 306-5) | 3, 9 | ||||

| Environmental conformity (compliance) | 9, 10, 14, 19 | ||||

| Assessment of environmental aspects regarding suppliers | 16 | ||||

| GRI 400: social topics 2016 | |||||

| Acea material Topics | Acea material Topics | Acea material Topics | |||

| Employment | 6, 7, 17 | Diversity and equal opportunities | 6 | Consumer health and safety | 2, 10, 12 |

| Industrial relations | 6 | Community life and local communities | 7, 8, 13, 15 | Marketing and labelling of products and services | 2, 10 |

| Health and safety at work | 5, 16 | Assessment of social aspects at supplier premises | 16 | Respect of privacy | 2, 10 |

| Training and education | 6 | Public politics (political contributions) | 10 | Socio economic compliance | 2, 10 |

NB: The economic, environmental and social “material aspects” were identified amongst all those provided for under the GRI standards (Topic-specific Standards).

When indicators are placed in brackets next to an aspect this means that only the indicators shown in the table will be considered material, or, where not specified, all the indicators related to the aspect are material (also see the GRI standard content index). For Acea material topics as identified in the table by a number, reference should be made to the figure illustrating the materiality matrix (Chart no. 1).

8 - It is important to consider that both the Topic-specific GRI standards — each of which includes a description of the management approach (Disclosure Management Approach) and a number of indicators — and Acea material topics both refer to contents that are far more complex and detailed than their brief name may suggest which, given their level of detail, cannot be presented at this time. See the GRI Standards — Consolidated set of GRI Sustainability reporting standards 2016 — in the website www.globalreporting.org.

9 - This led, for example, to the exclusion of topic-specific standards related to Presence on the Market and Human Rights which, according to the meaning given to them by the GRI, are more pertinent to multinational enterprises and not suited to the reality of the Group’s most significant operations.

10 - It is also important to note that some Acea material topics, already correlated to specific aspects of the GRI standards, are also consistent with some of the 56 general

standards (GRI 102: General Disclosures).

The principle of materiality was also applied to the definition of the “report scope”, as envisaged both by the standards adopted for reporting and by Legislative Decree no. 254/2016. The latter, in fact, under art. 4, states: “To an extent necessary for ensuring an understanding of the group’s activity, its performance, results and the impact it produces, the consolidated declaration includes data about the parent company, its fully consolidated subsidiary companies and covers the topics pursuant to article 3, paragraph 1”.

To identify the companies to be included in the report’s scope, the same approach was used as for the previous edition.

First of all, the adequacy of the criteria of strategic materiality/ significance – identified last year – was reconsidered and confirmed in order to identify the companies that ensure an understanding of the Group’s activities and its performance, taking into account the main business areas, the region where these activities are mainly carried out and the main impacts generated.

TABLE NO. 2 - COMPANIES INCLUDED IN THE PARENT COMPANY’S FULL CONSOLIDATION AREA (2018)

| COMPANY | REGISTERED OFFICE |

| Acea Ambiente Srl | Via G. Bruno, 7 – Terni |

| Aquaser Srl | P.le Ostiense, 2 – Rome |

| Bioecologia Srl | Via Simone Martini, 57 – Siena |

| Iseco SpA | Loc Surpian, 10 – Saint Marcel (AO) |

| Acque Industriali Srl | Via Bellatalla, 1 – Ospedaletto (PI) |

| Acea Energia SpA | P.le Ostiense, 2 – Rome |

| Acea8cento Srl | P.le Ostiense, 2 – Rome |

| Cesap Vendita Gas Srl | Via del Teatro, 9 – Bastia Umbria (PG) |

| Umbria Energy SpA | Via B. Capponi, 100 - Terni |

| Acea Energy Management Srl | P.le Ostiense, 2 – Rome |

| Parco della Mistica Srl | P.le Ostiense, 2 – Rome |

| Acea Dominicana SA | Avenida Las Americas – Esquina Mazoneria, Ensanche Ozama – Santo Domingo, Dominican Republic |

| Aguas de San Pedro SA | Las Palmas, 3 Avenida 20y 27 calle – San Pedro, Honduras |

| Acea International SA | Avenida Las Americas – Esquina Mazoneria, Ensanche Ozama – Santo Domingo, Dominican Republic |

| Acea Perù SAC | Calle Amador Merino Reyna – 307 Miraflores – Lima, Perù |

| Consorcio Acea-Acea Dominicana | Avenida Las Americas – Esquina Mazoneria, Ensanche Ozama – Santo Domingo, Dominican Republic |

| Consorcio Servicios Sur | Calle Amador Merino Reyna - San Isidro – Lima, Perù |

| Acea Ato 2 SpA | P.le Ostiense, 2 – Rome |

| Acea Ato 5 SpA | Viale Roma, snc – Frosinone |

| Acque Blu Arno Basso SpA | P.le Ostiense, 2 – Rome |

| Acque Blu Fiorentine SpA | P.le Ostiense, 2 – Rome |

| Crea Gestioni Srl | P.le Ostiense, 2 – Rome |

| Crea SpA (in liquidation) | P.le Ostiense, 2 – Rome |

| Gesesa SpA | Corso Garibaldi, 8 - Benevento |

| Gori SpA | Via Trentola, 211 – Ercolano (NA) |

| Lunigiana SpA (in liquidation) | Via Nazionale, 173 – Massa Carrara |

| Ombrone SpA | P.le Ostiense, 2 – Rome |

| Sarnese Vesuviano Srl | P.le Ostiense, 2 – Rome |

| Umbriadue Servizi Idrici Scarl | Strada Sabbione industrial area – Terni |

| Areti SpA | P.le Ostiense, 2 – Rome |

| Acea Illuminazione Pubblica SpA | P.le Ostiense, 2 – Rome |

| Acea Produzione SpA | P.le Ostiense, 2 – Rome |

| Acea Liquidation and Litigation Srl | P.le Ostiense, 2 – Rome |

| Ecogena Srl | P.le Ostiense, 2 – Rome |

| Acea Elabori SpA | Via Vitorchiano, 165 – Rome |

| Technologies for Water Services SpA | Via Ticino, 9 – Desenzano del Garda (BS) |

These criteria 11 include quantitative elements (such as the weight of turnover on the consolidated revenues, value of energy consumption expressed in TOE, etc.) and qualitative elements (companies having a relevant and current role in the Acea qualifying companies or an essential role respect to the services they provide; companies present in the territorial area in which almost all of the turnover is generated, the majority of the stakeholders is present and a large part of the managed assets is located). They were applied to the Companies included in the scope of consolidation of the Parent Company 2018 12 (see table no. 2) resulting in a scope proposal that, having heard the opinion of the Head of the Legal and Corporate Function of the Parent Company and the CFO, was shared with Top Management and communicated to the Ethics and Sustainability Committee.

The companies that are representative for the purposes of disclosing the 2018 non-financial information (in accordance with Legislative Decree no. 254/2016 and the GRI Standard) and therefore included in the scope of reporting 13, were the same as in the previous edition of the document (see table no. 3).

TABLE NO. 3 - CORPORATE SCOPE FOR THE ACEA GROUP SUSTAINABILITY REPORT 2018 (CONSOLIDATED NON-FINANCIAL STATEMENT PURSUANT TO LEGISLATIVE DECREE NO. 254/2016, PREPARED ACCORDING TO GRI STANDARD)

| COMPANY | REGISTERED OFFICE |

| Acea SpA | P.le Ostiense, 2 – Rome |

| Acea Ambiente | Via G. Bruno 7 Terni |

| Aquaser | P.le Ostiense, 2 – Rome |

| Acea Energia | P.le Ostiense, 2 – Rome |

| Acea8cento | P.le Ostiense, 2 – Rome |

| Acea Ato 2 | P.le Ostiense, 2 – Rome |

| Acea Ato 5 | Viale Roma, snc – Frosinone |

| Gesesa (*) | Corso Garibaldi, 8 – Benevento |

| Areti | P.le Ostiense, 2 – Rome |

| Acea Produzione | P.le Ostiense, 2 – Rome |

| Ecogena | P.le Ostiense, 2 – Rome |

| Acea Elabori | Via Vitorchiano, 165 – Rome |

(*) As far as Gesesa is concerned, the data regarding the areas of sustainability are progressively provided..

The scope of the Acea Group’s 2018 Sustainability Report is therefore consistent with what was defined the year before, guaranteeing continuity and comparability as well as coverage of the Companies that ensure full understanding of the Group’s activities and most significant sustainability performance. Furthermore, such companies represent at least: 90% of the turnover, 85% of the average number of employees and 85% of the costs for materials and services of the full consolidation area of Acea Group (including the Parent Company and excluding the companies that had entered that area in the last quarter of the year).

Lastly, in compliance with the principle of completeness required under GRI Standards, we considered it appropriate to provide qualitative and quantitative information regarding corporate and environmental matters also for certain companies, regardless of the method of consolidation, that are not included within the scope of the non-financial Statement. Specifically this concerns foreign activities and the following companies operating in the water area: Acque, Gori 14, Acquedotto del Fiora, Publiacqua and Umbra Acque, which were included in some Group data and described in a dedicated chapter, giving clear evidence of their individual contribution.

11 - Every considered quantitative element has defined thresholds of significance and elements of “non consistency” were also identified for qualitative criteria (such as “vehicle” companies, companies under liquidation with non-determining positions for the purposes of operativity, companies operating outside of the territory of reference, etc.). The conditions of contemporary presence of quantitative and qualitative factors were also established, aimed at defining the strategic significance of a company for the Group and its representative ability for the purposes of disclosing non-financial information.

12 - As required by Legislative Decree no. 254/2016.

13 - In light of the applied criteria, the following companies are outside of the scope of the Consolidated non-financial Statement 2018: Bioecologia, Iseco, Acque Industriali, Cesap Vendita Gas, Umbria Energy, Acea Energy Management, Parco della Mistica, Acea Dominicana, Aguas de San Pedro, Acea International, Acea Perù, Consorcio Acea-Acea Dominicana, Consorcio Servicios Sur, Acque Blu Arno Basso, Acque Blu Fiorentine, Crea Gestioni, Crea, Gori, Lunigiana, Ombrone, Sarnese Vesuviano, Umbriadue Servizi Idrici, Acea Illuminazione Pubblica, Acea Liquidation and Litigation, Technologies for Water Services.

14 - Gori was added to the scope of consolidation on a full basis in November 2018. Therefore, for the present reporting cycle it has not been considered within the scope of the Consolidated Non-Financial Declaration. See the section on Water Company data sheets and overseas activities.

Document structure and dissemination

In compliance with the implemented reporting Standards the Sustainability Report 2018 bears information and data mainly of a non-financial nature, with specific attention to social and environmental aspects of the managed activities.

The document is divided into three sections: Corporate identity, Relations with stakeholders and Relations with the environment, supplemented by the Environmental Accounts. The latter comprises about 400 items and parameters monitored which quantify the physical flows generated by the activities: the products, factors used (resources), outbound outputs (rejects and emissions) and some performance indicators.

It is important to note that where the document recalls the main economic-financial data and describes corporate governance, data and information are consistent with those given in the Consolidated Report and the Corporate governance report and which may derive from the latter.

The published data and information are provided by the Industrial Areas, Companies and responsible Functions (data owner), they are processed - and possibly reclassified with application of the reference Standards - by the internal workgroup which draws up the document and then submitted once again to the Areas/Companies/ Functions responsible for final validation, formalised by the issuing of a specific certificate.

Downstream of the audit activities by the appointed statutory auditor, the report distributed by means of publication in the institutional website - www.gruppo.acea.it - and the company intranet, as well as the other formats provided under Legislative Decree no. 254/2016 and the implementary Consob Regulation (implemented by Resolution no. 20267 of 19 January 2018). It is also distributed together with the consolidated Sustainability Report, by means of a dedicated kit: to the shareholders, during the annual Shareholders’ Meeting upon closure of the financial year, the directors and middle management of the Group and the interested public during events.

For further information about the Sustainability Report and its contents, it is possible to write to the following email address: RSI@aceaspa.it.

Giuseppe Sgaramella

SUSTAINABILITY UNIT

Antonio Sanna

RISK & COMPLIANCE FUNCTION